|

||

| The 2018 Tax Cuts and Jobs Act and 2025 OBBB for Creative People

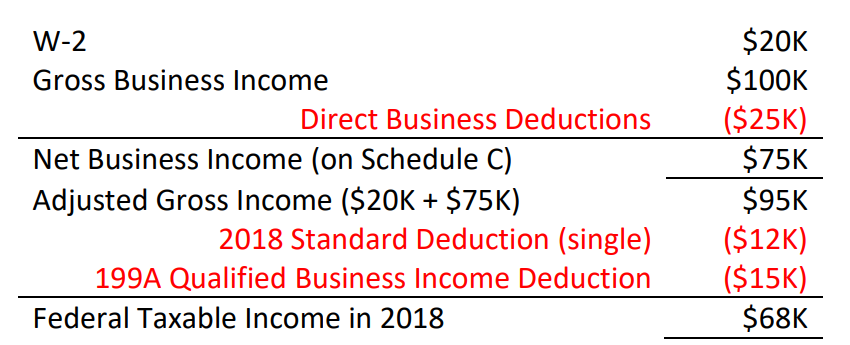

By, Peter Jason Riley, Certified Public Accountant There has been an astounding amount of misinformation regarding the new tax act and its effect on folks in the creative fields. Of course, there are many aspects of this new tax bill, both good and bad, that will impact all taxpayers such as the increased standard deduction, the elimination of personal exemptions and other provisions. The biggest gamechanger in the new tax bill for us is the new 20% business deduction (Section 199A). Simply put, this bill provides a new 20% “Qualified Business Income Deduction” calculated on your net business income. It does NOT replace your normal business deductions (wireless, rent, payroll, home office, meals, travel, supplies, etc.) but provides an additional deduction based on your net business income. For folks in creative fields there are 2 limitations in the calculation. Individuals in the arts are considered part of the laws “specified service businesses” and are thus limited to the 20% deduction but ONLY if their taxable income is less than $157,500 if single and $315,000 if married (after that is phases out over the next $50,000/$100,000 of taxable income). So, to use a simple example; if a single taxpayer, a musician, actor, visual artist or writer with a sole proprietorship has a net Schedule C income of $75K and a W2 of $20K. They will get a brand-new tax deduction equal to 20% of the $75K net business income, or in this case, $15K. The 2018 federal taxable income equation will look like this:

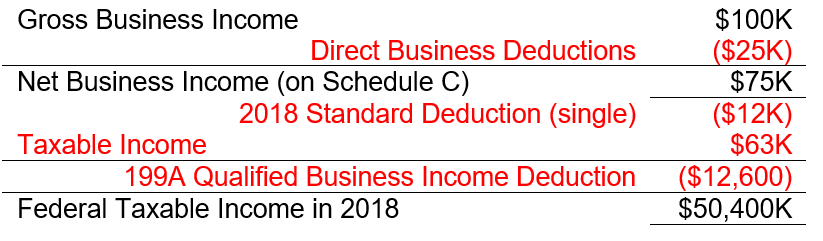

There is an additional cap to the 199A deduction, the deduction is limited to no more than 20% of taxable income, net of any capital gains income. If the taxpayer in our example did NOT have the additional W2 income shown above the 199A deduction would limited to $12.6K ($63K * 20%) and would look like this:

For a variety of reasons that are beyond the scope of our discussion here we see no reason to

set up a formal business entity, such as an LLC to take advantage of this new tax provision.

Please keep in mind that this is a VERY simplified overview of this complex law so make sure

you address these changes with your tax professional as you plan for 2018. The major change in the new tax bill is the elimination of the deduction for employee business

expenses (Form 2106). This is going to have a devastating effect for many employed

performers as Actors Equity, SAG-AFTRA and other organizations require that compensation be

paid on a W-2. As of 2018, these performers lose all ability to take their professional, out of

pocket expenses.

Musicians and Singers One of the key changes in the new tax bill is the elimination of the deduction for employee business expenses. While many successful musicians receive W2 income from touring gigs, they generally also have substantial income from self-employment for teaching, session work or private gigs. There has been no significant change in deductions for self-employed taxpayers; Schedule C stays virtually untouched. All direct business expenses for the musicians’ independent, free-lance (1099) work will keep all allowable deductions intact moving into 2018. Again, in 2018 the one change will be the inability to deduct expenses directly associated with W2 employment. In this case, the touring musician with significant out of pocket expenses related to W2 income would be better to receive lower compensation and have the touring company reimburse them their expenses. Writers

In our opinion, writers will see little or no change in the deductibility of their direct writing

expenses. A vast majority of independent writers are considered self-employed (remember,

writer royalties are considered earned/self-employment income for the creator) and there has

been no significant change in deductions for self-employed taxpayers; Schedule C stays virtually

untouched.

In our opinion, visual artists will see little or no change in the deductibility of their direct art

expenses. A clear majority of independent artists are considered self-employed (remember, an

artist’s income is considered earned/self-employment income for the creator) and there has

been no significant change in deductions for self-employed visual artists; Schedule C stays

virtually untouched. The OBBB signed by the president on July 4, 2025 extended the provisions discussed above. © Copyright 2001-2026 Riley Business Services 978.270.9260 All Rights Reserved |